{kind=link}

Romance. The idea alone tends to conjure up images of the modern “date night”. Spending cash to spend time together...

Maintaining healthy credit is a key factor in achieving financial success. This section will help you navigate your personal credit. We will review how your credit score is calculated and how lenders use this number determine your credit worthiness. With this knowledge, you will learn how to ensure your report and score are the most favorable they can be, as well as how to protect it.

A Little Background on Credit Reports and Scores

When you are issued a social security number, sometime right after you are born, the potential for your credit file to begin exists. Credit history is established the first time a credit account is reported to the credit bureaus by a lender for a person based on their name and social security number. The credit bureaus collect and store information about each credit account that is reported to them, usually on a monthly basis. This information generally includes the date the account was opened, current balances, credit limits, and a historical account of payment timeliness. Public records such as bankruptcies, liens, and judgments can also show up on your credit file. There are three major credit reporting agencies: Experian, Equifax, and TransUnion. These companies collect your credit file data based on the lender reporting it and create a report that’s updated monthly.

Your credit score is a three-digit number generated by an algorithm using data from your credit report. Each area weighs in numerically on your score in either positive or negative ways. This was designed to predict risk to a lender. The lower the score, the higher the risk, meaning there’s more likelihood for the borrower to default. While there are many different scoring models, the largest by far is the FICO credit score, which ranges from 300-850. Consumers have three FICO credit scores, one from each of the major credit bureaus. This is because not all lenders report to all three bureaus, so each report can contain different information. This is why your credit scores can vary by bureau.

Lenders typically use your credit reports, along with your credit score, to make lending decisions. This means that things like getting an apartment lease, getting utilities connected without a deposit, financing a vehicle, getting a mortgage, qualifying for a credit card, and everything in between is reliant on your credit history. It’s a big deal, and you’ll want to be as informed as possible about how to gain and keep a positive credit profile.

Healthy Credit From the Start

If you are just establishing your credit, the first thing you (and anyone on the path to taking control of their credit) should do it order your credit reports from each of the three major bureaus. Consumers are allowed one free report each year and can easily order it at www.annualcreditreport.com. This site will walk you through ordering your report from Equifax, Experian, and TransUnion. Most of the time your report will be available to you immediately, although sometimes you will be required to send in identification documents. Once you have the report and see that there is little to no activity, it’s time to begin building your credit. Here are some tips to ensure a solid foundation:

- Obtain a credit card that reports to each bureau. Because you have limited credit history, it may be difficult to get approved for an unsecured credit card. If you have a parent or family member willing to co-sign for you (who you trust to not use the credit themselves), this is one way to go. Another is to obtain a secured credit card. A secured card requires that you make a deposit of a certain amount, usually the credit limit. Most of these cards will return the deposit to you after several months of timely payments.

- Use the credit card, but do not pay off the entire balance each month. It seems counter-intuitive, but credit will generally build faster with a higher potential for positive score output when a small balance is left to revolve each month. Yes, you will likely have to pay interest on this amount (and, being a new borrower, it will likely be a high rate). The good news is that it shouldn’t be much. The percentage of credit you use relative to the amount of credit available is called referred to as your credit utilization rate. The “sweet spot” for positive credit score output for this area is around 10%. Meaning you should be paying all BUT 10% of your monthly credit card bill off. A great way to do this is to simply charge a full tank of gas or a round of groceries each month on your card. This keeps your monthly bill very manageable. And the small amount you do pay in interest is a small price to pay for building positive credit.

- Start with just one card. Opening many new lines of credit is a red flag on your credit report, and too many credit inquiries can also result in negative credit score output (more on this later). Adding another card every 6-12 months is a safe way to slowly build credit.

- Diversify your credit file by adding other types of accounts that report to the credit bureaus. The FICO credit score algorithm responds positively to files that have a mix of both credit and installment accounts on them (in good standing, of course). Installment accounts include car loans, student loans, and mortgage loans.

- Pay all of your bills ON TIME and do not allow any of your debts to go into collections. Something as small as an old unpaid utility bill is enough to severely damage your credit. The best advice a person new to the credit building world can receive is to always pay your bills on time and never, ever ignore a creditor. Pay close attention to medical bills, which are sometimes quickly referred to collections when not paid on time. Some of those collections stay on your credit report for seven years, even if you pay them.

- Sign up for credit monitoring and be vigilant about checking your credit at least quarterly. Credit monitoring and credit report pulls done through the bureau by you are considered “soft” pulls. These do not result in a documented inquiry on your credit file. Only “hard” pulls by lenders show up on your credit report and affect your score.

An In-Depth Look At How Your Score Is Calculated

The term “credit score” is a very general reference made to the three digit score we all know lenders use to determine our creditworthiness. But there isn’t just one score that comes from just one source. Your credit score is derived from the information contained in your credit report. But just like there isn’t just one credit report, there isn’t just one credit score. There are many companies that use many different credit scoring models. The company formally known as Fair Isaac Company developed the FICO score (the name being an acronym for the company name). They specialize in predictive analytics, which means they analyze data to come up with estimates about certain outcomes. In the case of the FICO score, they analyze data from your credit report to measure your risk of default. Lenders buy this score from FICO to determine your credit worthiness.

FICO sells several types of scores for all three major credit bureaus because each bureau may contain different information. So your scores may vary from bureau to bureau. Within the FICO score brand, there are several types of scores with slightly different number ranges, though the classic models carry a range of 300-850. There are several incarnations of scoring models made separately for the mortgage, auto, and bankcard industries. This means that your score may be different when pulled by an auto lender than when by an auto lender. In fact, each consumer has 65 different FICO scoring model scores. Most of these scores are only available to the lender.

Another credit score that has become popular amongst lenders is the VantageScore. VantageScore competes in the credit score market with FICO, although FICO still dominates a large portion of it. VantageScore is a joint venture of the three major credit bureaus and is one score that is calculated from information from all three. The numeric range is the same as FICO, 300-850.

The scores that you will get from credit monitoring sites will vary widely and will more than likely not be a FICO score, which you must purchase from FICO’s site. This isn’t usually necessary, though. One score that seems to consistently be closest to the score range lenders will see is the CreditXpert score. This is included in credit monitoring offered by reputable companies like Fifth Third Bank (https://www.53.com/personal-banking/identity-theft-protection/). Credit monitoring is a key element in protecting your credit and is worth the small monthly investment.

For more information about credit scores, the CFPB (Consumer Financial Protection Bureau) published a paper for the public about the differences between consumer and creditor-purchased credit scores which you can read here http://files.consumerfinance.gov/f/201209_Analysis_Differences_Consumer_Credit.pdf.

Credit Score Calculations

Your credit score is derived from one source, your credit file. Other information about your finances, like how much you earn, is not factored into your score. The algorithm’s used to calculate your score are highly secretive (remember, FICO and other scoring models are owned by private companies. These are not governmental programs; they are for profit industries). They have, however, been made to release the basic ways in which your score is weighed. These are generally broken down into five categories:

Payment history-35%

The element with the largest impact on your credit is your payment history. Your credit report is a seven-year history of your payment habits. Late payments are documented for the last seven years and even old ones have an impact. Items in collections, even those with a zero balance (with the FICO model, at least) are included in this category, as are public records like bankruptcies and judgements/liens.

Amounts owed-30%:

This is where your credit utilization comes in. How much you owe relative to how much available credit you have is a heavily weighted element of your credit score. This is why paying down a credit card with a high balance can have a very positive impact on your credit score.

Length of credit history-15%:

The older the account, the more positive the impact it has on your credit score. The best output in this category would be very old (five to seven years) accounts with no derogatory payment history. This is why it’s important to never close an old account, even if you aren’t using it. Keep it active and it will contribute both to this category of scoring and in your credit utilization. Even one and two-year-old accounts have positive output, though, and it’s a small slice of the collective pie. The more important piece is having no delinquencies.

Credit inquiries-10%:

When you pursue new credit, lenders will typically initiate a hard pull of your report and score. This results in an inquiry on your credit report that stays there for two years. Several inquiries combined with too many new accounts results in a negative output for your score. While it’s a small percentage, you want to avoid applying for new credit unless you really need it. The score does offer some leeway for consumers that are shopping for car loans or mortgages. In those instances, inquiries made within the same month will only have the impact of one inquiry.

Types of credit used-10%:

This refers to the mix of account types on your report. Having both revolving credit accounts, like credit cards, with some installment accounts, like car loans and mortgages, has some positive effect on your score. This element is pretty low impact, however, and shouldn’t cause a consumer to spend money on interest for a car loan or other installment loans if they are not needed.

It’s pretty clear that the two easiest ways to maintain good credit are to pay all of your bills on time and keep your credit utilization low. Having some utilization is important, as it creates revolving balances that give you the opportunity to have bills to pay on time each month. This furthers your potential for a longer positive credit history. Most credit experts agree that the “sweet spot” for credit utilization seems to be around 10%. This means on a card with a $5,000 limit, keeping a running balance of around $500 is a safe bet to get the most out of the scoring outputs.

You may be wondering what a good score is. Here’s a general guideline:

- “Poor” credit is anything less than 650

- “Fair” credit is within the range of 650-690

- “Good” credit is within the range of 701-759

- “Excellent” credit is anything above 760

While some people may still get credit extended to them with a score in the “Poor” range, the interest rates on the money they borrow will likely be much higher than those with “Good” or “Excellent” credit. Those people may find it difficult to secure a rental property or have utilities put in their name without a deposit.

The average American’s FICO score in 2015 was 695, which is on the high side of what’s considered “Fair” credit. That score will get most people a better rate than those with “Poor” credit, but not necessarily rates as low as advertised for mortgages, vehicles, and big ticket items. Scores in the “Good” range generally qualify buyers for the best-published rates on auto loans, but the best possible mortgage rates are usually reserved for people with “Excellent” credit.

How Much Does Negative Credit Affect Consumers?

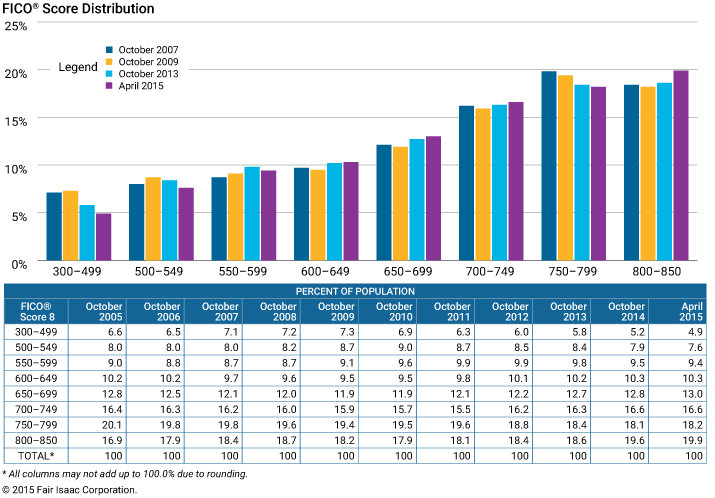

According to fico.com, more than 32% of Americans have a score lower than 650. This means that almost one-third of us have what is considered “Poor” credit (http://www.fico.com/en/blogs/wp-content/uploads/2015/08/April-2015-FICO-Score-Distribution.jpg). That’s 102 MILLION people that will struggle to obtain credit, get an apartment lease, finance cars, get insurance, and even get a job. If you find yourself in this situation, it’s obviously extremely common. There are many things you can do to begin the process of improving your credit. First, let’s take a hard look at the real cost of bad credit.

The obvious price people with a low credit score pay is in the cost of borrowed money. Higher interest rates equate to a ton of extra money spent compared to rates offered to what creditors consider more credit worthy borrowers (higher scores). The best example is a large debt paid off over a long period of time, like a mortgage. Let’s look at the comparison between what a person with “Poor” credit may pay for a home versus someone with “Good” credit.

Joe Smith has a “Poor” credit score of 620. He’s applied for a $200,000 on a thirty-year fixed mortgage. In all areas other than credit score, such as debt to income ratio, Joe is more than qualified for a mortgage. But his credit score hurt him in underwriting and the only mortgage he was offered carried a 4.88% interest rate. This means that over the thirty years, his monthly payments will be $1,060, and he will pay $181,247 in interest on the loan.

Jane Jones has a “Good” credit score of 720. She’s applied for the same $200,000 mortgage loan that Joe Smith did. She earns the same amount of money as he does and has the same debt to income ratio. Her credit score, however, has qualified her for an interest rate of 3.291%. This means that over the thirty years, her monthly payment will be $875 and she will pay $114,970.

Because of his lower score, over the life of the loan, Joe Smith will pay $66,277 more than Jane Jones pays. That’s a lot of money over 100 credit score points! But there’s even more at stake here for Joe. He’s paying almost $200 more each month for his mortgage than Jane. Imagine what he could do with that money? He’s missing the chance to invest it and make even more money. This lost opportunity is another cost consumer with lower credit scores pay.

People with lower scores are many times forced to buy used vehicles and mediocre appliances. They don’t qualify for new or top of the line items. These products usually require more maintenance and to be replaced more often, causing yet another financial burden on the consumer. Simply put, life with a low credit score can be an expensive drain.

Steps Towards Rebuilding Credit

Most negative credit remains on your report for seven years, and bankruptcy can stay there for up to ten. If you made mistakes in the past that negatively affected your credit, there are things you can do now to being repairing things now, but the time it will take and the results you will get depend on many factors, including the severity of your situation. The first thing you should do is order all three of your credit reports. You can do this for free, once each year, by visiting www.annualcreditreport.com. In most cases, you will receive your credit report immediately and can download and save it. Follow these steps once you receive your reports:

- Print them out and review each one closely for errors. Your credit score is based solely on information from these reports. In 2012, the FTC released a study finding that one in five consumers had errors on their credit reports (https://www.ftc.gov/news-events/press-releases/2013/02/ftc-study-five-percent-consumers-had-errors-their-credit-reports). There are consumer protection laws in place that require transparency in reporting. Even the smallest late pay or collection error can result in big credit point losses. If you find errors, experts suggest never to dispute them online, as you may unknowingly waive some of your rights to dispute them in the future. The process of disputing errors can be labor intensive, but it’s extremely important to be vigilant about ensuring that only accurate information be contained in your reports.

- Pay down high balances wherever you can. Remember that 30% of your credit score is based on your credit utilization. If you have cards that have high balances relative to their limits, this is likely hurting your score. You can usually see a boost in as little as two to three months by simply paying those cards down to around 10% of the available credit. This means if you have a card that has a $5,000 limit, pay it down so that you owe somewhere close to $500. This is the second largest factor in determining your score, so keeping your utilization around 10% on all accounts is a great way to boost your score.

- If the severity of your situation was such that accounts were closed and you no longer have open credit lines, now is a good time to start over with a secured credit card. These typically require a deposit and come at a higher interest rate, but you should keep to the 10% rule and never let your balance roll over with more than that percentage of your available credit being used. This should mean minimal interest charges. Be sure to check with the credit card company to ensure that they report to all three of the major bureaus.

- If you have a trusted family member or friend that is willing to help you through this process, getting them to co-sign for a loan or credit card is a great way to add additional positive lines of credit to your report. This is obviously a big favor, as this person’s credit will be affected negatively if you don’t make the payments on time. Make sure that you have the ability to be responsible with the account if someone is willing to help you in this way.

The process of rebuilding your credit can be extremely frustrating. Some people choose to use do it yourself programs as a tool to restore their credit. While this can be effective, it can also be extremely time consuming and should be reserved for people with the time and means to dedicate towards this endeavor. There’s also the option to get professional help through the Credit Correction Solution. This type of assistance can help you with many more strategies for correcting and rebuilding your credit.

Identity Theft

According to the Bureau of Justice Statistics, an estimated 17.6 million American’s were victims of identity theft in 2014 (http://www.bjs.gov/content/pub/pdf/vit14_sum.pdf). We often think about the monetary loss associated with identity theft. Thieves steal your credit card information and rack up fraudulent charges that create a big mess. Even when you can get your money back, the time and energy spent spearheading the effort can be devastating. The lesser discussed repercussions of identity theft are the ways it can affect your credit report and score. Scammers can open new credit lines in your name that are obviously never paid. If you aren’t checking your reports regularly, you may very well never even know it’s happening until your credit is ruined.

Here are some ways to protect yourself against identity theft:

- When shopping online, always ensure you are doing business with a reputable company. The internet is full of elaborate scams that involve stealing payment information at virtual check outs. Look for the padlock icon next to the website’s URL. Be sure the company is rated with the BBB and has plenty of reviews from previous shoppers. Never buy anything online when connected to the internet via Public Wi-Fi.

- While this may seem archaic, it’s still best to shred up documents with your personal information on them before recycling the paper. Old fashioned garbage picking thieves still exist, and sometimes all they need is a bank statement or tax document to get what they want

- Password protect all of your devices and update your virus protection regularly. Be sure to choose strong passwords that contain a mix of character cases and numbers. Never use your personal information, like date of birth or social security number, as your password. It’s also a good idea to change your passwords regularly. Log out of your internet sessions when you are done, even on your home computer.

- Be smart when giving out your personal information. Banks will almost never ask you to provide sensitive information by e-mail, so always question when it appears that they are. There are very elaborate scams that make e-mails and even snail mail appears to be coming from legitimate financial institutions. Always call your financial institution to check if what they are requesting is in fact from them.

- Only keep the credit and/or debit cards you use in your wallet. This is an easy way to minimize the potential for theft. If your wallet is stolen, you will obviously want the least amount of opportunity available to the thief. This will make reporting the theft much easier on you, as you will only have to contact a few of your credit card companies.

- Be proactive about checking your credit card statements and credit reports. Credit card fraud is such a successful crime because many people never find out they’ve been stolen from. Checking the transactions on your credit card statements ensures that you know only you have been using the card.

Identity Theft

Between the potential for identity theft and the potential for errors on your credit report, it’s more important than ever to be proactive about monitoring your credit files. The first step in protecting your credit is to know what is being reported, and electronic credit monitoring is a fantastic way to streamline that process. Many financial institutions offer credit monitoring for free to their customers. If yours doesn’t, banks like Fifth Third Bank offer reliable credit monitoring for about $15/month (https://www.53.com/personal-banking/identity-theft-protection/) <find out about affiliate referral programs for this or others and replace where we can monetize> Maintaining reliable credit monitoring is a key element in protecting your credit. Always pull your full credit reports each year (www.annualcreditreport.com).

You are the front line to build and maintain positive credit and to protect it. The most important thing you can do is stay engaged with this process on a consistent basis. Remain vigilant about staying on top of your credit through monitoring it with any of the several tools available to you. By now you know how important your credit is to the success of your financial life and beyond.

Feeling overwhelmed? Help is available for many common financial problems!

Recent Articles

Save Cash on Child Care Costs

Childcare costs are one of the largest expenses a family with children will face. This is especially true for single...

Stay Tuned for More Articles!

Articles on Credit and Debt, Personal Finance, and Education are coming soon! Check back frequently.

Tips to Save on Groceries

According to The Department of Labor, the average American spends 12.4% of their income on food. Up to 47% of...